"And I beheld, and lo a black horse; and he that sat on him had a pair of balances (weighing-scales) in his hand."

When a corporate financial news source features an interview on their homepage from a financial investment CEO who says "I recommend prayer," it is time to sit up and pay attention to what may be about to happen.

The Bank of England, and Credit Suisse, as well as many other banks worldwide are on the verge of collapse.

The rich rulers of the world, who profit off of unfair trading - driving entire nations into poverty [banks], have dropped the snowball down the mountain, which will grow into an avalanche the likes of which the world has never seen.

Some headlines this week around the globe:

Eurozone facing 'severe risks' to financial stability, admits ECB

The eurozone’s financial system is facing “severe risks” from the chaos gripping global markets, the European Central Bank said in an unprecedented warning as Germany unveiled a €200bn (£177bn) borrowing binge.

Meanwhile, Spain’s socialist-led government agreed a temporary wealth tax to fund its efforts to fight the crisis. People with a fortune of more than €3m would be taxed at 1.7pc, rising to a rate of 3.5pc for those with more than €10m.

The darkening economic outlook and the sliding value of investments are the major threats to the eurozone financial system.

The regulator also sounded the alarm on rising mortgage rates threatening the housing market and the growing threat of cyber attacks on banks in the wake of Russia’s invasion of Ukraine.

Bank of England intervenes to restore financial stability

The British government’s shift toward fiscal stimulus recently upended British financial markets. The combination of massive energy subsidies and tax cuts alarmed investors who worried that the British budget deficit would become unsustainable.

The International Monetary Fund (IMF) urged the British government to “re-evaluate” its fiscal program and suggested that the new policy could intensify inflation.

So far, the government has been publicly unrepentant. As for the BOE, if investors start to believe that it will fund future government deficits, then the decision to purchase bonds could ultimately backfire, leading to renewed crisis.

Inflation continues to accelerate in Europe

Inflation in the 19-member Eurozone continues to accelerate, largely due to the energy crisis. In September, consumer prices were up 10% from a year earlier (the first double-digit increase ever) and were up 1.2% from the previous month. Energy, and to a lesser extent food, played the dominant role in driving inflation.

Energy, and to a lesser extent food, played the dominant role in driving inflation. Energy prices were up 40.8% from a year earlier and up 3% from the previous month.

The inflation is mostly being driven by the political tug of war between Russia and the EU regarding the flow of natural gas.

Spanish banks need to boost provisions amid slowdown, De Cos says

"The potential impact of the current uncertain environment on the banking sector requires extreme caution. Banks will have to increase their provisions to cover potential losses," De Cos told a financial event in Madrid.

Britain on the brink of a social explosion after pound’s collapse

Former Bank of England Governor Mark Carney said

The main threat he identified was the immediate need to safeguard government bonds and pension funds from being “unable to make short-term obligations… that would cascade through financial markets.”

Former Bank of England Deputy Governor Sir Charlie Bean warned, “Frankly, the only way you can really deal with this is with a very fundamental rethinking of the boundaries of the state…

How to Turn the Tables on Tyrants Waging the Economic War

The Federal Reserve has ordered another 'super-sized interest hike' in what appears to be a hopeless effort to contain runaway inflation.

The Federal Reserve recently ordered another “super-sized interest hike” — the fifth rate hike this year — in what appears to be a hopeless effort to contain runaway inflation.

Cost of food rising 10.9% in the last 12 months. Overall, energy prices have seen the highest increases, rising by 41.6% between June 2021 and June 2022.

Financial crisis historian Adam Tooze predicts several crises may converge over the next six to 18 months, including food crises, energy crises, pandemic outbreaks, stagflation, a Eurozone sovereign debt crisis and potential nuclear war

"During banking crises, you won’t have full access to your deposits in the bank. As a result, electronic payments such as bank cards may become useless. In the extreme case, your deposits could be used to recapitalize ailing banks in a process called 'bail-in.'"

People have already begun to report banks declining withdrawls from theirown personal and business accounts, as google, youtube and the gatekeepers have "disappeared" many of these videos.

The Prophecies warn of what is going to happen to the rich rulers of the Earth, and the Churches, who have worked with the rich to keep the masses in the dark; down and poor , by helping the rich to hide God's PERFECT Laws and substitute the rich people's oppressive and illegal laws.

This world is run by a small group of EXTREMELY rich jews who are known as "TheHidden Hand ". They say they are Jews and are NOT . They are the "synagogue of Satan " (Rev. 3 v 9).

These same people had already been previously condemned as traitors by God through Jeremiah in the third chapter of Jeremiah - note well verses 9-11 - "Treacherous Judah ".

UK Prime Minister Liz Truss showed no sign of backing down on her economic policies that yesterday forced a dramatic £65 billion intervention from the Bank of England, blaming Russia’s war in Ukraine for the market turmoil that pushed the pound to a record low.

“I’m very clear the government has done the right thing,” she said Thursday in a round of interview to local BBC radio stations. “This is the right plan.”

The remarks were Truss’s first since the £45 billion of unfunded tax cuts were unveiled six days ago. The central bank was forced to step in and buy gilts as a week of market upheaval left many pension funds facing margin calls. The British currency fell after the comments before later rebounding. The price of government debt also fell as Truss spoke, before paring losses.

Truss has made the most turbulent debut of any British prime minister in peacetime. In just three weeks, her administration has been battered by a crisis of confidence in her policies that have triggered a collapse in the pound and a surge in borrowing costs that threaten to push the UK toward a deep recession and a housing market crash.

The pound traded as much as 1.2% lower, but was up 1.8% at $1.1082 as of 5:18 p.m. in London.

It was the first time Truss has publicly addressed the market turmoil, which was sparked Friday when Chancellor of the Exchequer Kwasi Kwarteng announced the largest package of unfunded tax cuts in half a century.

These strategies require cash collateral to be held with an LDI manager; more cash may need to be added in response to market moves. Last week’s sharp spike in long-term bond yields (which mean a fall in bond prices) saw pension funds using LDI strategies face unprecedented demands for more cash. Schemes that could not meet these calls risked defaulting or having their hedging positions closed.

Is UK's financial disaster a warning to the world?

Rupee hits record low of 82 against US dollar after OPEC+ plan production cut

The Indian rupee hit a record low of 82.22 against the dollar on Friday as rising oil costs and a strong dollar index dampened investor confidence.

The rupee had previously reached a session low of 81.88. Traders will now be intently examining US payrolls report to gain a new understanding of the country's inflationary pressures.

Following recovery from a two-week low, the dollar index, which measures the value of the dollar against a basket of six significant rival currencies, was barely changed at 112.032.

In light of rising commodity costs, the World Bank on Thursday reduced India's GDP projection for this fiscal year by a whole percentage point.

The weakness of the Asian equities markets today followed the overnight lower finish on Wall Street. The benchmark Sensex index for the Indian stock market fell more than 250 points in early trade.

“Traders will be concerned as the World Bank projected a growth rate of 6.5 per cent for the Indian economy for the fiscal year 2022-23, a drop of one per cent from its previous June 2022 projections, citing the deteriorating international environment," said Mohit Nigam, head, PMS, Hem Securities, reported Live Mint.

Brent crude futures were trading at or above $94.31 a barrel and were expected to post significant weekly gains.

Beginning in November, the Organization of Petroleum Exporting Countries and its partners want to cut production by two million barrels per day.

However, because some countries are pumping far less than their mandates, the real-world drop will probably be between 1 million and 1.1 million, according to Saudi Arabia's oil minister.

If oil prices rise higher, analysts predict greater currency depreciation.

2nd FDIC-Insured Bank in 3 Days COLLAPSES! Bank Runs, Trading Halted on Some Banks

Silicon Valley Bank became the second FDIC-insured bank to collapse in 3 days today. They are reportedly the 16th largest bank in the U.S., and the largest bank to collapse since the 2008 financial meltdown, and the second largest bank to ever collapse in the U.S.

While it was still not the main headline news this morning in the corporate media, a glance at the headlines as I began to write this article shows that it is apparently now getting the headline news it should receive, as bank runs are starting, and some banks suspended trading today to stop the carnage.

First, the FDIC took over Silicon Valley Bank (SVB) today. And just a reminder, the FDIC only insures accounts up to $250,000.

Only 2.7% of Silicon Valley Bank deposits are less than $250,000. Meaning, 97.3% aren't FDIC insured. Ouch.

Silicon Valley Bank, one of the tech sector’s favorite lenders, is shutting down.

The California Department of Financial Protection and Innovation announced Friday that it was taking over and closing the distressed bank to protect deposits, naming the Federal Deposit Insurance Corporation as its receiver. The FDIC has formed a separate entity where all insured SVB deposits are being transferred.

The closure marks the biggest bank failure since the 2008 financial crisis and the second-largest on record after Washington Mutual collapsed during that industry-wide meltdown, according to FDIC data.

Like other FDIC-member banks, deposits are insured up to $250,000 per depositor. The agency said it is “working over the weekend” to determine how many SVB deposits are insured.

The shutdown came after a tumultuous morning for the Santa Clara, California-based bank — the 16th largest bank in the country — during which trading of its shares was halted after they fell by double-digits before markets opened. That downslide came on the heels of a more than 60% decline Thursday.

In view of the tumult, Treasury Secretary Janet Yellen told House lawmakers Friday morning, “There are recent developments that concern a few banks that I’m monitoring very carefully, and when banks experience financial loss it is and should be a matter of concern.” (Full article.)

This news has led to a dramatic drop in value in trading for ALL banks, and several of them reportedly suspended trading on the NYSE for a while today. Bank runs have also been reported.

Shades of 1930’s. This is my bank in Wellesley this morning. Boston Private Bank, recently acquired by Silicon Valley Bank. Ruh, roh.

Venture Capital firms who held accounts at SVB are panicking. The Information reports:

Startups and VCs Scramble to Pay Employees After SVB’s Collapse

The sudden collapse of Silicon Valley Bank sowed panic at hundreds of startups and venture capital firms that banked there and now must seek new ways to pay employees and access funds from their investors and customers.

Founders and VC firms, which also kept billions of dollars worth of assets with SVB, on Friday rushed to figure out whether they could get loans to cover payroll if their funds were still tied up in the bank, which a federal banking regulator took under receivership on Friday.

“The reality is sinking in among founders who are realizing, ‘I have payroll this week and I’m not able to log into my SVB account right now.’ And maybe the money will be there in the future, but they need it right now,” said Billy Libby, CEO of startup debt and equity investor Upper90.

The scramble highlighted Silicon Valley Bank’s deep connections with the tech industry. Besides clients that deposited cash or took out loans from the bank, hundreds of startups and dozens of venture capital firms had received investments from the bank’s venture capital arm.

Its startup portfolio includes crypto compliance firm Chainalysis and credit card startup Jeeves, PitchBook said. Many VC firms, including Andreessen Horowitz and Kleiner Perkins, have also held their money at the bank, according to PitchBook.

One startup founder said they had about $10 million in an SVB checking account when the bank failed. The company’s finance team is now trying to open a new bank account and use the company’s Treasury bills and other securities to pay vendors and employees.

“I am talking to people whose only bank account was at SVB and they are trying to figure out how to make payroll. That’s a true statement. That’s scary for a lot of people,” said Andy Boyd, who used to lead tech investing at Fidelity Investments and now runs Bramalea Partners, a VC firm. (Full article - Subscription required.)

Which Banks are Next?

Bank Stocks Plummet as Bank Runs in the U.S. Gain Momentum at Federally-Insured, Non-Traditional Banks

If you keep a diary or news journal, be sure to write down March 9, 2023 as the day that a full-blown bank run began at non-traditional banks in the U.S.

Bank depositors were already nervous after federally-insured Silvergate Bank (ticker SI) announced on Wednesday evening that it was closing and liquidating. Its publicly-traded stock had already lost over 90 percent of its market value over the prior 12 months at that point.

Now, for the second time in less than two weeks, depositors are panicking over the fate of another federally-insured bank. This time it’s Silicon Valley Bank (ticker for holding company is SIVB) which, like Silvergate Bank, had become a go-to bank for a special niche customer. Instead of crypto, its niche was venture capital outfits and private equity firms.

Silicon Valley Bank is not a small bank. According to its regulatory filings, as of December 31 it held $161.4 billion in domestic deposits and $13.9 billion in foreign deposits. (Full article.)

Crypto bank Signature slides on Friday amid troubles at Silicon Valley Bank, Silvergate

Signature Bank shares dropped as much as 32% on Friday and were at one point halted amid a sell-off in bank stocks that continued for a second day.

Signature, one of the main banks to the cryptocurrency industry, was last down by 24%.

The initial move followed a big day for its crypto banking peer Silvergate Capital, which announced earlier this week that it would liquidate its bank. Its losses deepened Thursday after shares of SVB Financial, whose Silicon Valley Bank lends to tech startups, announced a plan to raise more than $2 billion in capital to help offset losses on bond sales.

By late Friday morning, the Federal Deposit Insurance Corp had closed Silicon Valley Bank and taken control of its deposits, making it the largest U.S. bank failure since the global financial crisis.

First Republic Bank, PacWest Bancorp, Western Alliance Bancorp were among the other names whose trading was at one point halted for volatility.

Signature has said it has minimal exposure to crypto, but Silicon Valley Bank's need to recapitalize on the heels of the Silvergate event has linked the two events in some people's minds.

Valkyrie chief investment officer Steve McClurg said the Signature Bank was already hurting on the back of Silvergate's losses, which now total almost 50% for the week. Its Friday losses are a spillover effect from the Silicon Valley Bank woes, he added.

Ed Moya, an analyst at Oanda, emphasized Signature is caught in the middle of both narratives.

"Signature Bank is getting hit with a one-two punch as concerns grow that any crypto-related bank could be in danger and as financial instability concerns grow for parts of the banking sector," he said. "There are only a handful of publicly traded banks that have crypto exposure and lots of traders are rushing to bet against them." (Full article.)

Signature Bank is not the only bank being mentioned, however. Market Watch identified 20 other banks with "huge potential securities losses" like SVB.

20 banks that are sitting on huge potential securities losses—as was SVB

Silicon Valley Bank has failed following a run on deposits, after its parent company’s share price crashed a record 60% on Thursday.

Trading of SVB Financial Group’s stock was halted early Friday, after the shares plunged again in premarket trading. Treasury Secretary Janet Yellen said SVB was one of a few banks she was “monitoring very carefully.” Reaction poured in from several analysts who discussed the bank’s liquidity risk.

California regulators closed Silicon Valley Bank and handed the wreckage over to the Federal Deposit Insurance Administration later on Friday.

Below is the same list of 10 banks we highlighted on Thursday that showed similar red flags to those shown by SVB Financial through the fourth quarter. This time, we will show how much they reported in unrealized losses on securities — an item that played an important role in SVB’s crisis.

Below that is a screen of U.S. banks with at least $10 billion in total assets, showing those that appeared to have the greatest exposure to unrealized securities losses, as a percentage of total capital, as of Dec. 31.

Corrupt Banking Industry Infection Spreading to Other Markets

SVB failure triggers shockwaves across biotech industry

Silicon Valley Bank’s failure has sent shockwaves across the biotech industry and spurred a panic among top venture capital firms, some of whom have confirmed to Fierce Biotech that they have urged their companies to withdraw deposits.

Nearly half of all U.S. venture-backed technology and life science companies bank with SVB—the 16th largest bank in the country—with a total of $342 billion in client funds and $74 billion in total loans.

Vida Ventures Co-Founder and Managing Director Arjun Goyal, M.D., said in an interview with Fierce Biotech that the firm has advised companies to examine their exposure to SVB and transfer that to other banks.

Goyal did not explicitly mention the companies that were advised, but Vida has invested in biotechs such as Volastra Therapeutics, Alterome Therapeutics, Capstan Therapeutics and Aktis Oncology in the past year. (Full article.)

The Information is reporting that the infection has also spread to China

The panic over the status of Silicon Valley Bank intensified on Friday, as the stock of SVB’s parent fell another 66% in pre-trading hours. Meanwhile, anxieties spread to China overnight, prompting local venture capitalists and entrepreneurs to follow their U.S. counterparts and look for alternative banks for their U.S. dollar holdings.

The fate of SVB is a huge concern in China, the world’s second-largest venture capital market after Silicon Valley, because SVB was among the first financial institutions to start catering to Chinese startups when traditional banks shunned them. The bank established its first Chinese arm nearly two decades ago,

“Silicon Valley Bank has played an instrumental role for us,” said Guanchun Wang, founder of Laiye, a Beijing-based enterprise software startup. “We opened our first bank account with them when the likes of Citi wouldn’t have anything to do with us.” (Full article.)

Is this the Start of Consolidating the Banking Industry to Replace the Monetary System with Central Bank Digital Currencies?

Corporate executives at Silicon Valley Bank are being criticized today because they allegedly sold over $4.4 million in stocks two weeks ago, suggesting that they knew ahead of time what was coming and that their bank was going to fail.

Silicon Valley Bank CEO, CFO and CMO sold +$4.4MM in stock over the last 2 weeks.

This liquidity crisis is due mainly to the Fed's policies of driving up interest rates, and if more bank runs are going to take place, which seems most likely at this point, which banks are going to be the ones that suffer the most?

Smaller, local regional banks are the ones that could easily be driven out of business, or swallowed up by the larger banks.

And while this article does not address the issue of rolling out CBDCs, it explains very well why the smaller, local regional banks are the ones most in trouble right now.

Which boils down to the following: if depositor confidence in the regional/small bank sector is now shot - and after both Silvergate and SIVB it very well may be - we will see a small (to medium if not larger) deposit run among the regionals which could prove devastating for these reserve-constrained bankswhich will need to scramble to raise capital a la SIVB in what eventually transforms into a death spiral for the sector, especially if depositors take one look at what is going on with regional bank prices - which have been in freefall in the past two days - and extrapolate what may come next - there's a reason why banking is the ultimate confidence game.

There is one way to short-circuit this process and it, of course, involves the Fed which would need to step in the way it did in September 2019 when it was the big banks - namely JPMorgan - that were reserve-constrained, and forced the Fed to launch "Not QE" (but only after the US repo market suffered some historic rollercoaster moves). Ironically, even if the Fed does somehow whisper words of reassurance, the question is why would depositors park their money at "suddenly" risky banks when they can just buy a 6M T-Bill and get the same return with zero risk.

Yes, the Fed may have no choice but to cut rates if it wishes to save the (regional) banking system. But then again, the Fed is still stuck fighting runaway inflation, which means that Powell is now trapped, and as we tweeted previously, Powell is now trapped: More hikes: regional banks collapse; Less hikes: inflation target must be raised.

So will Powell let America's small, regional banks risk failure as a result of his rate hikes (an outcome the likes of JPMorgan would find quite beneficial as it will make them even bigger), or will the Fed chair step in the way he did in 2019 even if it means gambling with runaway inflation? The right answer to that question could make some traders extremely rich.

The entire article is well worth reading at ZeroHedge News.

“We’ve got strong financial institutions…Our markets are the envy of the world. They’re resilient, they’re…innovative, they’re flexible. I think we move very quickly to address situations in this country, and, as I said, our financial institutions are strong.” – Henry Paulson – 3/16/08

“I have full confidence in banking regulators to take appropriate actions in response and noted that the banking system remains resilient and regulators have effective tools to address this type of event. Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out . . . and the reforms that have been put in place means we are not going to do that again.” –Janet Yellen – 3/12/23

With the recent implosion of Silicon Valley Bank and Signature Bank, the largest bank failures since 2008, I had an overwhelming feeling of deja vu. I wrote the article** Is the U.S. Banking System Safe** on August 3, 2008 for the Seeking Alpha website, one month before the collapse of the global financial system. It was this article, among others, that caught the attention of documentary filmmaker Steve Bannon and convinced him he needed my perspective on the financial crisis for his film Generation Zero. Of course he was pretty unknown in 2009 (not so much anymore) , and I continue to be unknown in 2023.

The quotes above by the lying deceitful Wall Street controlled Treasury Secretaries are exactly 15 years apart, but are exactly the same. Their sole job is to keep the confidence game going and to protect their real constituents – the Wall Street bankers. And just as they did fifteen years ago, the powers that be once again used taxpayer funds to bailout reckless bankers. Two hours before the only solution the Feds know – print money and shovel it to the bankers – Michael Burry explained exactly what was about to happen.

When Biden, Yellen, and the rest of the Wall Street protection team tell you the banking system is safe and they have it under control, they are lying, just as I said fifteen years ago.

“Our economy and banking system is so complex and intertwined that no one knows where the next shoe will drop. Politicians and government bureaucrats are lying to the public when they say that everything is alright. They do not know. Should you believe a governmental agency that wants the public to remain in the dark to avoid bank runs, or an independent analysis based upon balance sheet analysis?”

Back in the days of The Big Short, before the public knew about toxic subprime mortgages issued by criminal bankers and packaged into derivatives given a AAA rating by the greedy compliant rating agencies, the Wall Street cabal knew time was growing short, but that didn’t keep the lying bastards like John Thain (Merrill Lynch), Dick Fuld (Lehman Brothers), Angelo Mozilo (Countrywide), Kerry Killinger (Washington Mutual), and others from pretending their institutions were healthy and profitable – right up until the day they collapsed. Lying is in the DNA of every financial executive, politician, government bureaucrat, and Federal Reserve hack.

The quote from Hemingway seemed pertinent in 2008 and is just as pertinent today.

Why the Failure of Credit Suisse is such a big deal; It was a "Bulge Bracket Bank"

To average, everyday people, the failure of Credit Suisse is simply some news headline. They have no clue at all what this means: ALERT - Time's up. Why? Because Credit Suisse was a "Bulge Bracket Bank." You may know it better as "too big to fail." But fail it has.

What is a bulge bracket bank?

A bulge bracket bank refers to a top-tier, multinational investment bank that has a leading role in the global financial markets. The term "bulge bracket" originally referred to the banks listed at the top of the "league tables" for securities underwriting, but it has since come to encompass a wider range of financial services.

Bulge bracket banks typically have a strong presence in both the domestic and international markets, providing a broad range of services such as underwriting, M&A advisory, equity and debt offerings, and sales and trading of securities. They also typically work with large, high-profile clients such as corporations, governments, and institutional investors.

Examples of bulge bracket banks include Goldman Sachs, JPMorgan Chase, Morgan Stanley, Bank of America Merrill Lynch, Citigroup, and Deutsche Bank. These banks are known for their extensive resources, large-scale operations, and high-profile deals.

What banks are considered bulge bracket?

Some of the banks that are considered bulge bracket are:

JPMorgan Chase & Co.

Goldman Sachs Group, Inc.

Morgan Stanley

Bank of America Merrill Lynch

Citigroup, Inc.

Deutsche Bank AG

rclays PLC Credit Suisse Group AG In fact, UBS Group AG

Wells Fargo & Co.

These banks are considered bulge bracket because they typically have a leading role in the global financial markets and provide a wide range of financial services to large, high-profile clients such as corporations, governments, and institutional investors. They are also known for their extensive resources, large-scale operations, and high-profile deals.

What would happen if a bulge bracket bank failed?

If a bulge bracket bank were to fail, it could have serious repercussions on the global financial system and the broader economy. This is because these banks are deeply interconnected with other financial institutions and play a significant role in the global financial markets.

If a bulge bracket bank were to fail, it could trigger a domino effect that would lead to other financial institutions experiencing financial distress or failing. This could lead to a credit freeze, where access to credit is severely restricted, making it difficult for businesses and individuals to obtain financing. This, in turn, could lead to a slowdown in economic activity and a recession.

To prevent such a scenario, regulators have put in place various measures to monitor and regulate the activities of bulge bracket banks. For example, these banks are subject to more stringent capital and liquidity requirements, stress tests, and other regulations to ensure their financial stability and resilience. In the event of a failure, regulators may also intervene to stabilize the financial system and protect the broader economy from the fallout of a bank failure.

Credit Suisse Failed

Those measures do NOT seem to have worked. Reverberations from the Credit Suisse failure, and the utterly vicious zeroing of Credit Suisse "Tier A1" Bonds, is starting to spread.

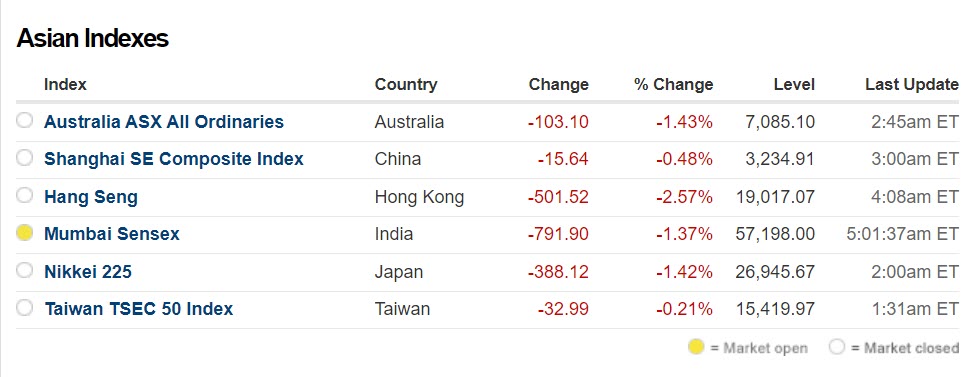

As this story is written at 4:45 AM on 20 March 2023, Asian Stock Markets have almost completed their trading day. They're all in the red:

Credit Suisse, $CS, was worth $10 billion a month ago and sold for pennies on the Dollar.

The government said $CS had “serious risk of bankruptcy.”

A shareholder vote was bypassed.

Regulators knew it was a matter of hours for bankruptcy.

This deal was made out of desperation.

In fact, the "rescue" was not a rescue. UBS could only work an equity trade, they themselves lacked the cash for a real buyout! That deal was total clown world.

Stock Markets know this. Stock Holders are learning of it now. The markets will begin to react TODAY.

Europe is opening shortly. That's where we will see some of the Credit Suisse fallout.

In the Asian Markets HSBC & Standard Chartered both down 6%.... will be interesting to watch the European markets when they open.

US markets open in about 3.5 hours. As Europe goes, so will the US.

You see, those "Tier 1A "Bonds that were Zeroed for Credit Suisse . . . they totaled slightly over seventeen billion dollars. Somebody has now lost all that money. Well, a lot of somebody's, actually.

That loss is going to have an impact. Maybe an impact on someone big. And that may take THEM out.

Moreover, the zeroing of Tier 1A Bonds just showed bondholders all over the world, that when it comes to BANKS, their "totally secure" Tier 1A bonds, aren't nearly as secure as they were lead to believe! People are going to start dumping those bonds, because clearly, they're now far riskier than anyone ever thought.

When you factor-in the reality that the Swiss government changed their law in real-time, to prevent Credit Suisse stockholders from having the Statutory 6 weeks to consider a merger or buyout offer, the bondholders (and Stock holders) now know they're sitting ducks. They have NO PROTECTION of law. The "rules" went right out the window.

As these Bond holders (and maybe stock holders) run for the exits today - and this week - their selling is going to put the banks under even MORE pressure.

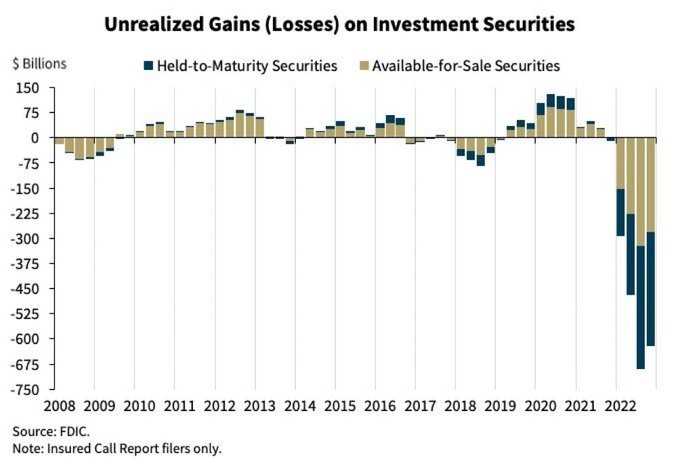

In the US, here's how fragile the banks actually are:

At the far right of the chart is this year - right now. As you can see, the banks are stuck holding Bonds that are worth LESS than their face value. In the color gold, those bonds can be sold by the banks if the banks need to raise cash. Those gold-colored (sellable) bonds are worth three-hundred BILLION dollars LESS than their face value.

As long as the banks don't have to sell them (to raise cash) the loss on the bond is "unrealized." But as people begin to take more money out of the banks, because the general public sees the banks as untrustworthy, some banks are going to HAVE TO sell those bonds. And the moment they do, the loss becomes "realized" and the bank is in trouble.

This week may very well be historic. We just don't know how it will turn out.

Politicians all over the world are screaming from the rooftops that "the banks are safe and secure." Trouble is, the public long ago learned that when they tell you things are safe, that's when you run!

Because politicians and government officials have shown themselves to be liars, over and over , and over again. Only the truly stupid believe them anymore.

With that reality, there's no telling what will happen this week. However . . . Calamity . . . is on the menu.

This isn't going away.

This is not your typical msm-driven race-baiting, class warfare, type of drivel designed to distract you from real problems.

This is a real problem. They're going to try to keep your eyes - and mind - off of it with crap like North Korea nuclear threats, Trump's impending arrest, etc. Expect some race-fueled incident to really throw everyone over the edge.

If they can keep us worked up over things like that, maybe we won't notice all the banks failing and the economy literally crumbling around us. Maybe.

This isn't something they can bury and hide for long, though, but they will try to keep us in the dark as long as possible. Many won't notice until bank failures and sky-high inflation impacts them personally.

When they know you notice the real problem, like with the Credit Suisse-UBS merge, they'll issue some statement about how all is well and good, the US dollar is strong and we shouldn't worry. When they say this kind of nonsense is when you need to worry the most.

UPDATE 5:20 AM EDT --

European market:

UBS - 12%

Deutsche -10%

most others -8%

people do not believe their lies anymore . . . this is a bad omen for everything today . . . .

There are numerous key Deep State agendas moving forward amid the ongoing banking crisis that is rearing its head in America and beyond, warns The New American magazine's Alex Newman in this episode of Behind The Deep State. From helping Democrats and establishment forces centralize money and power, to paving the way for bigger government and Central Bank Digital Currencies (CBDCs) and even censorship of the Internet, this mess has Deep State fingerprints all over. Alex explains how there are obvious parallels with what happened in the Great Depression: First, flooding the economy with low-interest credit, then sucking the money out of the system, crashing everything, and scooping up assets for pennies on the dollar. Perhaps even more importantly, Newman breaks down how the Federal Reserve System works and how this was engineered.

President of Kenya Urges Citizens To Get Rid of U.S. Dollars - soon (Operation Sandman????)

The President of Kenya today announced to all citizens they should get rid of any U.S. Dollars they may be holding because they will become worth less within weeks.

William Kipchirchir Samoei Arap Ruto, Ph.D, CGH; is a Kenyan politician who is serving as the fifth and current president of Kenya since 13 September 2022.

Prior to becoming president, he served as the first deputy president of Kenya from 2013 to 2022.

Today, in a nationally televised speech in Kenya, Ruto said “Those of you who are holding dollars, you shortly might go into losses. So you better do what you have to do because this market will be different in a couple of weeks.”

This stunning announcement gives credibility to a RUMOR that has been circulating for over a year, that 142 countries around the world have secretly agreed to what they call "Operation Sandman."

According to the RUMOR, Operation Sandman will "put the US Dollar to sleep" by having all 142 countries repudiate the currency on the same day, and refuse to continue accepting it for payment in Trade.

Countries around the world began planning this when they witnessed the then-Democrat-Controlled US Congress, go on a spending spree of several TRILLION Dollars in Omnibus Bills. Those countries realized there is nothing backing the value of US Dollars and they saw that the US Congress has no plans at all to reign-in spending.

One country's Finance Ministry recently told the US, "We are no longer willing to accept ones and zeros in a bank computer as actual payment for real goods."

The countries agreed that holding US currency was becoming foolish because it was becoming worthless on its face, thanks to all the rampant over-spending by the US Government.

Now, it appears those countries may actually take action "within a couple weeks."

If countries around the world repudiate the Dollar as payment for goods in trade, then they would halt providing manufactured goods or raw materials unless paid in some currency OTHER THAN DOLLARS.

Since the U.S. barely does any manufacturing at all anymore, thanks to the business nitwits who thought it was a good idea to convert the US economy to a "service economy" then products we buy in stores will simply run out and we will be unable to re-stock because no one will want our money.

Among the business nitwits are also those who pushed for "Free Trade" claiming it would improve sales of American-made goods overseas if America agreed to halt Tariffs on all imported items. The government bought-into the idea, not realizing - or not caring - that these very businessmen weren't at all interested in selling more American goods overseas. What they were interested in was shipping American JOBS overseas, taking advantage of cheap labor, then shipping those exact same products back to the USA to sell at the same high prices . . . . while pocketing the profit from the new, foreign, cheap labor without having to pay Tariiffs.

The Businessmen, their corporate Boards of Directors, and Commerce Organizations who touted "Free Trade" were the ones who moved American jobs overseas and now, the country barely manufactures anything, anymore.

So here we are, years later, and thanks to those businessmen, and the federal politicians who foolishly believed their lies about "Free Trade," we have almost no manufacturing. Countries around the world seem to be actually planning to stop accepting the US dollar as payment, so we won't be able to buy anything because it's all made overseas now!

Retaliation against the people who did this should be swift and ferocious when Americans can no longer buy even life's basics because corporate titans and certain others stripped our country of manufacturing.